Mutual Fund Portfolio: 5 Essential Funds You Should Add

30th May 2019

Building mutual fund portfolio is very much similar to building a house; different types of materials to use, various designs, tools, and strategies, but each structure shares some basic features.

With a bunch of schemes offered by the mutual fund houses left serious long term investors thoughtful which fund to include in their portfolio. Listed below are five such funds which helps investors to make ideal mutual fund portfolio; this is just like the basic structure of any investor’s core portfolio.

Good Read: Indian Stock Market Journey from 100 to 40000 Points

Diversified Equity Mutual Fund

If mutual funds are the best investment option for small and retail investors to invest in shares, diversified equity funds are by far the most cost-efficient. A large-cap fund with a sound track record should be part of every small investor’s core portfolio. This can be further classified into following.

Investor Category |

Funds to Choose |

Aggressive Investor |

Midcap fund |

Aggressive + Low-risk Investor |

Multicap Fund |

Low-risk Investor |

Index Fund |

Diversified equity funds invest in the stocks of the index they track and hence their returns are not very different from those of the index. But in the last 5 years, the average diversified equity fund has outperformed the broader market by 4% to 5% points. (This is the average return and some funds have also underperformed the market)

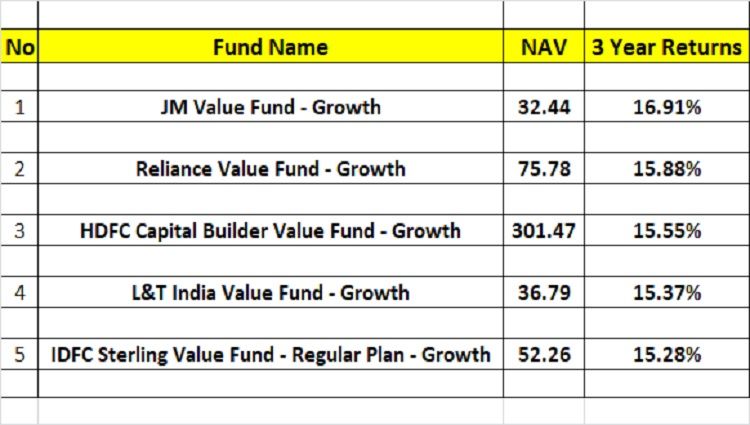

5 best-performed Diversified Equity Funds

Equity Linked Saving Scheme (ELSS) Fund

An Equity Linked Saving Scheme (ELSS) Funds serves many purposes of the investor’s portfolio. It

(1) Save tax up to 1.5 lakh under section 80C

(2) Offers exposures to equities and

(3) Provide regular income by way of dividend

The ELSS category is the tax-saving option with the shortest lock-in period of 3 years. It is the lock-in period which differentiates ELSS funds from other diversified equity funds. It likewise allows the fund manager to line the portfolio with stocks that may not reap immediate results but could be rewarded if held for a long period of time.

Must Read: Mutual Funds Investing: 4 Tips Can Make You Millionaire

Before you take the plunge, remember that you will not be able to withdraw your investment before 3 years. Also, systematic and long-term investment in well-managed ELSS fund or diversified mutual fund can create huge wealth for you. This can also be a blessing in disguise for investors who tend to withdraw too soon or get jumpy when the market turns volatile.

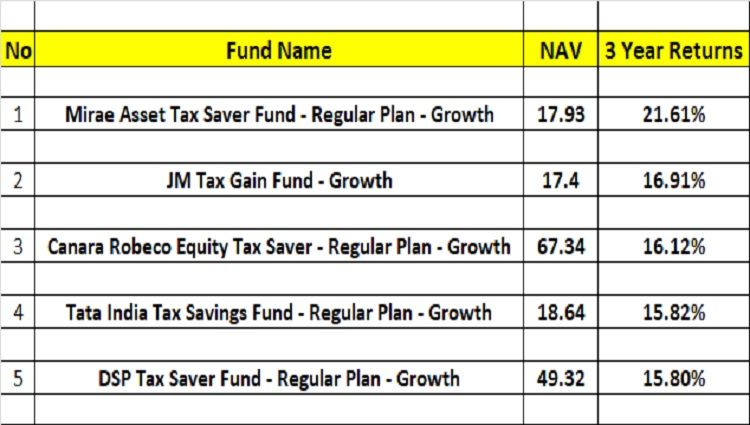

5 best-performed ELSS Funds

Gold Fund

Physical gold offers a great advantage to the buyer because he/she can use it even as an when its value appreciates. If the investors’ purpose is purely an investment, gold ETFs is a better option.

Gold Fund Advantages

-

No making charges

-

Very high liquidity

-

Investors don’t have to bother about storage

-

Allow investors to accumulate gold in small quantities

-

Eligible for long-term capital gains if holds for 1 year and more

Short-Term Equity Fund

As the name suggests, short-term income funds are a good way to save for short and medium term goals. They are liquid (easily sold and money can be reached in bank account within a day)

Advantages of Investing in Income Funds

Higher returns compare to FDs: Income funds generally generate returns higher than fixed deposits in the long term. Do keep in mind that income funds do carry credit risk and interest rate risk whereas FDs carry negligible or zero risk.

High Liquidity: Unlike some fixed deposits, income funds do not have any lock-in period and allow investors to anytime withdraw their investment (exit loads may be imposed for redemptions in these funds from 1 to 3 years)

Tax Efficient: Income funds are tax efficient than fixed deposits, especially for those investors who fall in the income tax brackets of 30 percents.

Read: 7 Mistakes Every Small Equity Investor Often Commits

Fixed Maturity Plan (FMP)

A fixed maturity plan (FMP) is a closed-ended debt scheme that invests in corporate bonds, commercial papers (CPs), certificate of deposits (CDs), money market instruments, and bank deposits (they do not invest in equities) matching the tenure of the scheme. Same as short-term income funds, an FMP is a tax-efficient replacement for fixed deposits.

Who should invest in FMPs?

Fixed maturity plans are ideal for those investors, who need returns higher than a regular FDs but can accept the frequent NAV (price) fluctuations. Compared to equity funds, FMPs are low risk-low return investments.

Like debt fund, the profit is treated as long-term gain after one year and taxed at a lower rate of 10 percent or 20 percent after indexation. Investors can claim indexation benefit if the holding period is 2 or more financial year.

Also Read

Value Pick Stock May 2019: Sharda Cropchem Limited

Disclaimer: The contents and data presented here are just for your information & personal use only. While much effort is made to provide the information, I ( Vishal Dalwadi ) or “FinBlab” do not guarantee the accuracy, correctness, completeness or reliability of any information or data displayed herein and shall not be held responsible.

Tags: Diversified Equity Funds, ELSS Funds, Fixed Maturity Plan, Gold Fund, ideal mutual fund portfolio, Investor’s Core Portfolio, Mutual Fund Portfolio, Portfolio, Short-Term Equity Fund